The NFIB Research Foundation has collected Small Business Economic Trends data with quarterly surveys since the 4th quarter of 1973 and monthly surveys since 1986. Survey respondents are drawn from NFIB’s membership. The report is released on the second Tuesday of each month. This survey was conducted in March 2024.

Small Business Optimism Index

March 2024 Report:

Small Business Optimism Reaches Lowest Level Since 2012

The NFIB Small Business Optimism Index decreased by 0.9 of a point in March to 88.5, the lowest level since December 2012. This is the 27th consecutive month below the 50-year average of 98. The net percent of owners raising average selling prices rose seven points from February to a net 28% percent seasonally adjusted.

“Small business optimism has reached the lowest level since 2012 as owners continue to manage numerous economic headwinds,” said NFIB Chief Economist Bill Dunkelberg. “Inflation has once again been reported as the top business problem on Main Street and the labor market has only eased slightly.”

Key findings include:

- The net percent of owners who expect real sales to be higher decreased eight points from February to a net negative 18% (seasonally adjusted).

- Twenty-five percent of owners reported that inflation was their single most important problem in operating their business (higher input and labor costs), up two points from February.

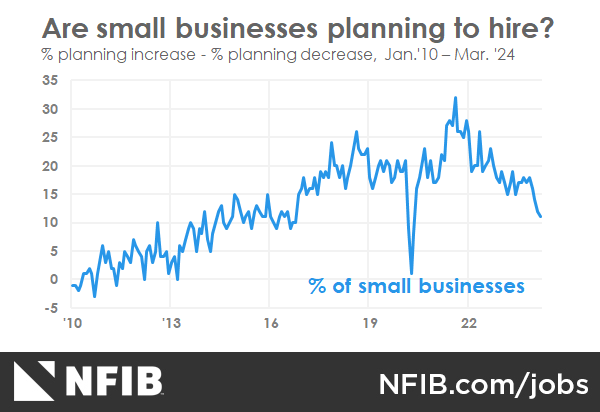

- Owners’ plans to fill open positions continue to slow, with a seasonally adjusted net 11% planning to create new jobs in the next three months, down one point from February and the lowest level since May 2020.

- Seasonally adjusted, a net 38% reported raising compensation, up three points from February’s lowest reading since May 2021.

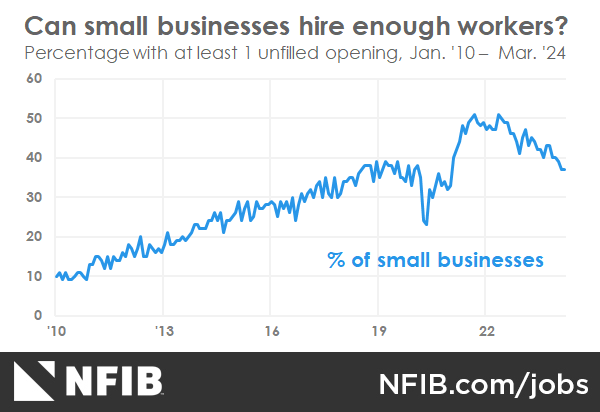

As reported in NFIB’s monthly jobs report, 37% (seasonally adjusted) of all owners reported job openings they could not fill in the current period. A net 21% (seasonally adjusted) plan to raise compensation in the next three months, up two points from February. The percent of small business owners reporting labor quality as their top small business operating problem rose two points from February to 18%. Labor cost reported as the single most important problem for business owners decreased by one point to 10%, only three points below the highest reading of 13% reached in December 2021.

Fifty-six percent of owners reported capital outlays in the last six months, up two points from February. Of those making expenditures, 38% reported spending on new equipment, 24% acquired vehicles, and 17% improved or expanded facilities. Ten percent of owners spent money on new fixtures and furniture and 5% acquired new buildings or land for expansion. Twenty percent (seasonally adjusted) plan capital outlays in the next few months.

A net negative 10% of all owners (seasonally adjusted) reported higher nominal sales in the past three months, up three points from February. The net percent of owners expecting higher real sales volumes declined eight points to a net negative 18% (seasonally adjusted).

The net percent of owners reporting inventory gains fell six points to a net negative 7%. Not seasonally adjusted, 12% reported increases in stocks (down one point) and 22% reported reductions (unchanged). A net negative 5% (seasonally adjusted) of owners viewed current inventory stocks as “too low” in March, down one point from February. A net negative 7% (seasonally adjusted) of owners plan inventory investment in the coming months, unchanged from February.

The net percent of owners raising average selling prices rose seven points from February to a net 28% seasonally adjusted. Twenty-five percent of owners reported that inflation was their single most important problem in operating their business, up two points from last month.

Unadjusted, 13% reported lower average selling prices and 43% reported higher average prices. Price hikes were the most frequent in finance (61% higher, 10% lower), retail (54% higher, 6% lower), construction (51% higher, 4% lower), wholesale (50% higher, 17% lower), and transportation (44% higher, 0% lower). Seasonally adjusted, a net 33% plan price hikes in March.

The frequency of reports of positive profit trends was a net negative 29% (seasonally adjusted), up two points from February, but still a very poor reading. Among owners reporting lower profits, 29% blamed weaker sales, 17% blamed the rise in the cost of materials, 13% cited usual seasonal change, and 12% cited price change. For owners reporting higher profits, 53% credited sales volumes, 23% cited usual seasonal change, and 12% cited higher selling prices.

Two percent of owners reported that all their borrowing needs were not satisfied. Twenty-seven percent reported all credit needs met and 59% said they were not interested in a loan.

A net 8% reported their last loan was harder to get than in previous attempts. Four percent of owners reported that financing was their top business problem. A net 17% of owners reported paying a higher rate on their most recent loan, up one point from February.

The NFIB Research Center has collected Small Business Economic Trends data with quarterly surveys since the fourth quarter of 1973 and monthly surveys since 1986. Survey respondents are randomly drawn from NFIB’s membership. The report is released on the second Tuesday of each month. This survey was conducted in March 2024.

LABOR MARKETS

Thirty-seven percent (seasonally adjusted) of all owners reported job openings they could not fill in the current period, unchanged from February and the lowest reading since January 2021. Thirty-one percent have openings for skilled workers (down 1 point) and 14 percent have openings for unskilled labor (up 2 points). The difficulty in filling open positions is particularly acute in the transportation, construction, and services sectors. Job openings in construction were down 9 points from last month. Openings were the lowest in the finance and wholesale sectors. Owners’ plans to fill open positions continue to slow, with a seasonally adjusted net 11 percent planning to create new jobs in the next three months, down 1 point from February and the lowest level since May 2020. Overall, 56 percent reported hiring or trying to hire in March, unchanged from February. Forty-eight percent (86 percent of those hiring or trying to hire) of owners reported few or no qualified applicants for the positions they were trying to fill (down 3 points). Twenty-nine percent of owners reported few qualified applicants for their open positions (up 4 points) and 19 percent reported none (down 7 points). Reports of labor quality as the single most important problem for business owners increased 2 points to 18 percent. Labor cost reported as the single most important problem for business owners decreased 1 point to 10 percent.

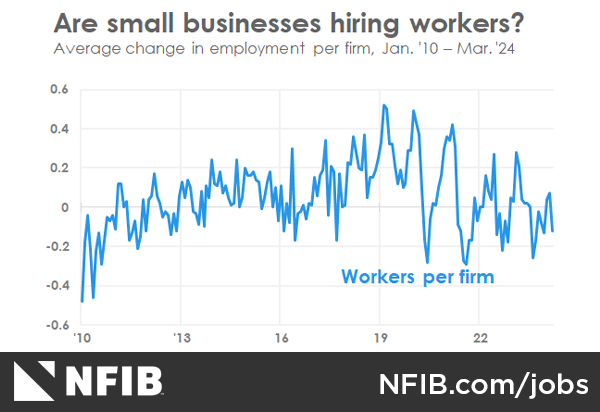

Click images to view

CAPITAL SPENDING

Fifty-six percent reported capital outlays in the last six months, up 2 points from February. Of those making expenditures, 38 percent reported spending on new equipment (up 3 points), 24 percent acquired vehicles (up 1 point), and 17 percent improved or expanded facilities (up 2 points). Ten percent spent money on new fixtures and furniture (down 2 points) and 5 percent acquired new buildings or land for expansion (down 1 point). Twenty percent (seasonally adjusted) plan capital outlays in the next few months, down 1 point from February. A more positive view of the future economy and economic policy would help stimulate longer term investment spending, but currently, owners’ views about the future are not supportive and financing costs are very high. Investment is needed to address labor supply chain problems which still persist in the current environment.

INFLATION

The net percent of owners raising average selling prices rose 7 points from February to a net 28 percent seasonally adjusted. Twenty-five percent of owners reported that inflation was their single most important problem in operating their business (higher input and labor costs), up 2 points from February. Unadjusted, 13 percent (down 3 points) reported lower average selling prices and 43 percent (up 6 points) reported higher average prices. Price hikes were most frequent in the finance (61 percent higher, 10 percent lower), retail (54 percent higher, 6 percent lower), construction (51 percent higher, 4 percent lower), wholesale (50 percent higher, 17 percent lower), and transportation (44 percent higher, 0 percent lower) sectors. Seasonally adjusted, a net 33 percent plan price hikes in March (up 3 points).

CREDIT MARKETS

Two percent of owners reported that all their borrowing needs were not satisfied, down 1 point. Twenty-seven percent reported all credit needs met (up 3 points) and 59 percent said they were not interested in a loan (down 2 points). A net 8 percent reported their last loan was harder to get than in previous attempts (up 1 point). Four percent reported that financing was their top business problem (unchanged). A net 17 percent of owners reported paying a higher rate on their most recent loan, up 1 point from February. The average rate paid on short maturity loans was 9.8 percent, up by 1.1 points from last month. Twenty-eight percent of all owners reported borrowing on a regular basis, up 3 points from the previous month.

COMPENSATION AND EARNINGS

Seasonally adjusted, a net 38 percent reported raising compensation, up 3 points from February’s lowest reading since May 2021. A seasonally adjusted net 21 percent plan to raise compensation in the next three months, up 2 points from February. Ten percent cited labor costs as their top business problem, down 1 point from February and only 3 points below the highest reading of 13 percent reached in December 2021. Eighteen percent said that labor quality was their top business problem (up 2 points). The frequency of reports of positive profit trends was a net negative 29 percent (seasonally adjusted), up 2 points from February. Among owners reporting lower profits, 29 percent blamed weaker sales, 17 percent blamed the rise in the cost of materials, 13 percent cited usual seasonal change, and 12 percent cited price change. For owners reporting higher profits, 53 percent credited sales volumes, 23 percent cited usual seasonal change, and 12 percent cited higher selling prices.

SALES AND INVENTORIES

A net negative 10 percent of all owners (seasonally adjusted) reported higher nominal sales in the past three months, up 3 points from February. The net percent of owners expecting higher real sales volumes deteriorated 8 points to a net negative 18 percent (seasonally adjusted). The net percent of owners reporting inventory gains fell 6 points to a net negative 7 percent. Not seasonally adjusted, 12 percent reported increases in stocks (down 1 point) and 22 percent reported reductions (unchanged). A net negative 5 percent (seasonally adjusted) of owners viewed current inventory stocks as “too low” (e.g. inventories are too large) in March, down 1 point from February. A net negative 7 percent (seasonally adjusted) of owners plan inventory investment in the coming months, unchanged from February.

COMMENTARY

The small business sector is showing signs of a potential slowdown in economic activity with net sales expectations falling 8 points, the main contributor to the decline in last month’s Index. However, continued stress in navigating inflation pressures leads as the top business problem. Inflation continues to frustrate owners as a significant share of them still report it as their biggest problem in operating their business. The Federal Reserve has taken notice, with a shift in dialog among some on the FOMC. The 2024 schedule of anticipated rate cuts have dropped precipitously over the last few months from a possible 6-7 cuts, to 2-3 cuts…maybe. The Minneapolis Federal Reserve President Neil Kashkari has even suggested the possibility of suspending rate cuts entirely this year, moving the first cut until 2025. The data are certainly not supportive of cuts at the next two FOMC meetings. Cuts at those meetings are off the table. The BLS reported 303,000 jobs added to the labor market in March. No signs of labor weakness there (but watch for revisions), although 71,000 did come from the public sector, mostly at the local level. One half of the Fed’s mandate looks good, the other half still frustrating Main Street. In the meantime, small businesses will have to manage higher financing costs a bit longer.

Just knowing NFIB is on your side is cause for optimism

Let’s chat for 10 minutes and we’ll help you understand all the ways NFIB is advocating for you and your business.