Small Business Optimism Index

Small Business Optimism Index

March 2026

The NFIB Research Foundation has collected Small Business Economic Trends data with quarterly surveys since the 4th quarter of 1973 and monthly surveys since 1986. Survey respondents are drawn from NFIB’s membership. The report is released on the second Tuesday of each month. This survey was conducted in March 2026.

Small Business Optimism Fell in March Survey

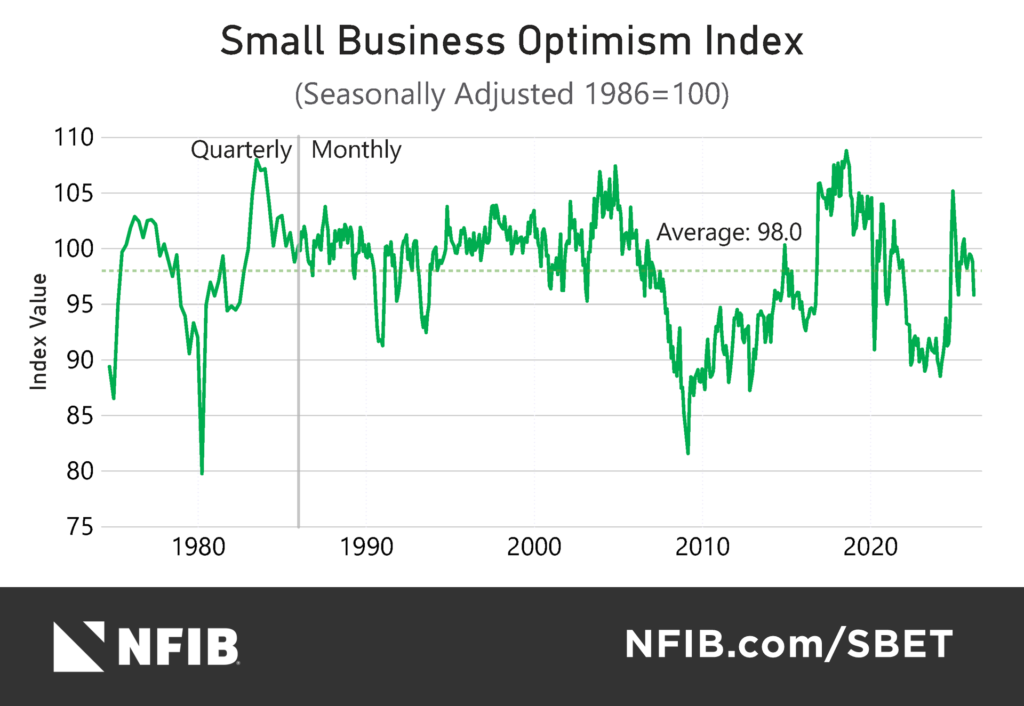

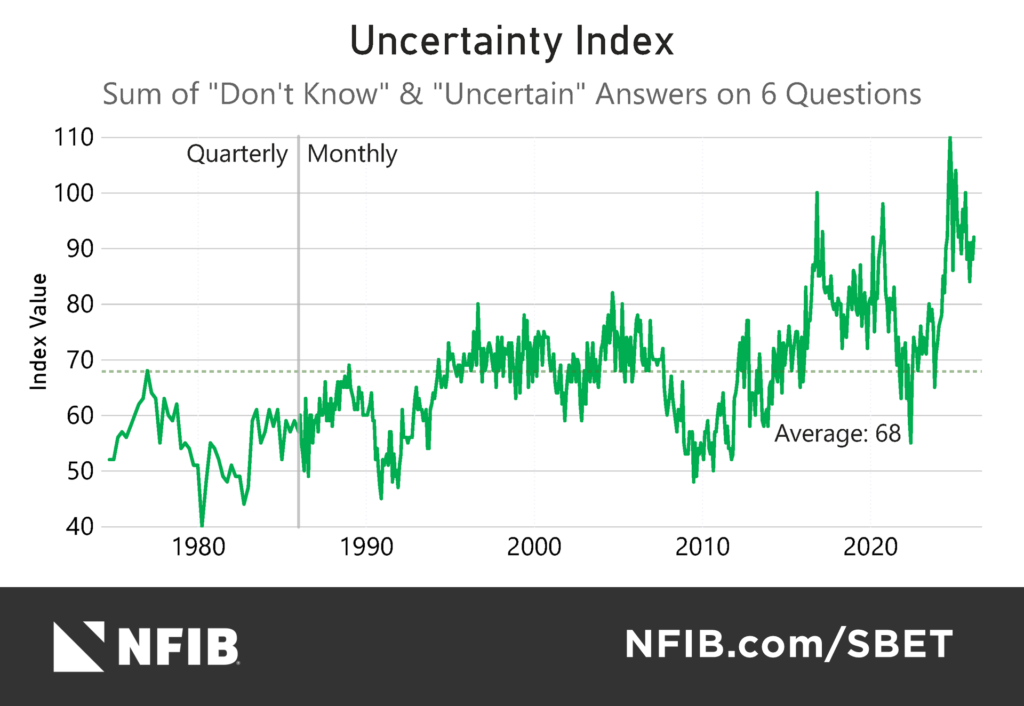

The NFIB Small Business Optimism Index fell 3.0 points in March to 95.8, leaving it below its 52-year average of 98.0. The last time the Optimism Index fell below its historical average was April 2025. The Uncertainty Index rose 4 points from February to 92, well above its historical average of 68.

“The 20% Small Business Deduction and other supportive small business tax provisions in the Working Families Tax Cut Act have had many positives for small business owners,” said NFIB Chief Economist Bill Dunkelberg. “However, the dramatic spike in oil prices has spooked consumers and owners alike. Small business owners are having to absorb those higher input costs and pass them along to their customers.”

Key Findings:

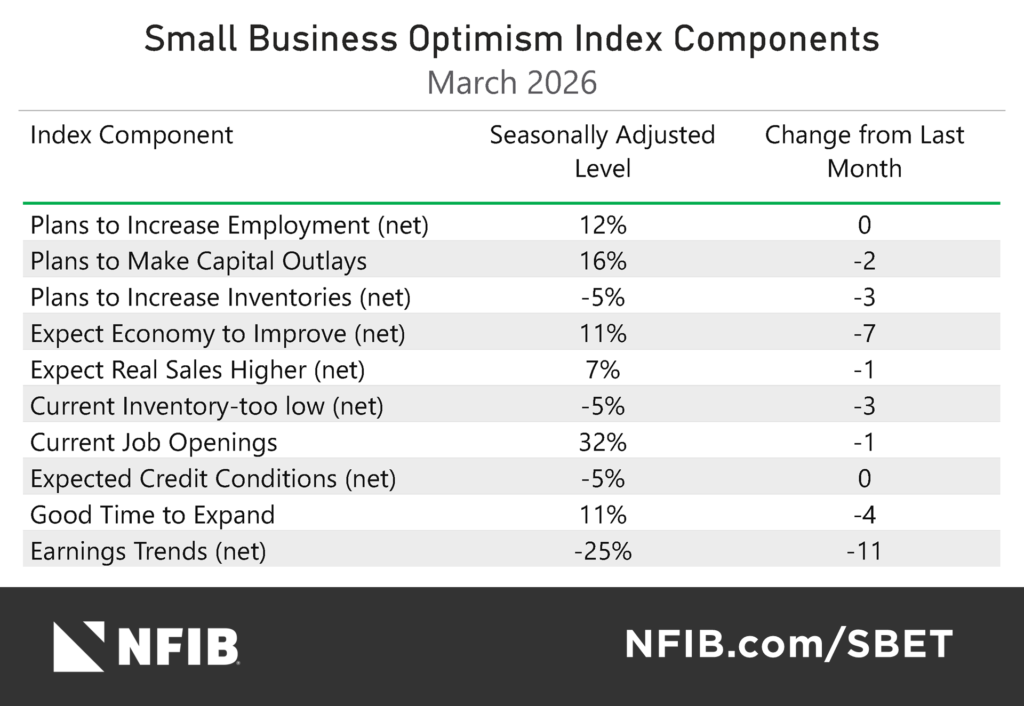

The frequency of reports of positive profit trends fell 11 points from February to a net negative 25% (seasonally adjusted), contributing the most to the Optimism Index’s decline.

The net percent of owners expecting better business conditions fell 7 points from February to a net 11% (seasonally adjusted), the third consecutive monthly decline and the lowest level since October 2024. This was the second biggest contributor to the Index’s decline.

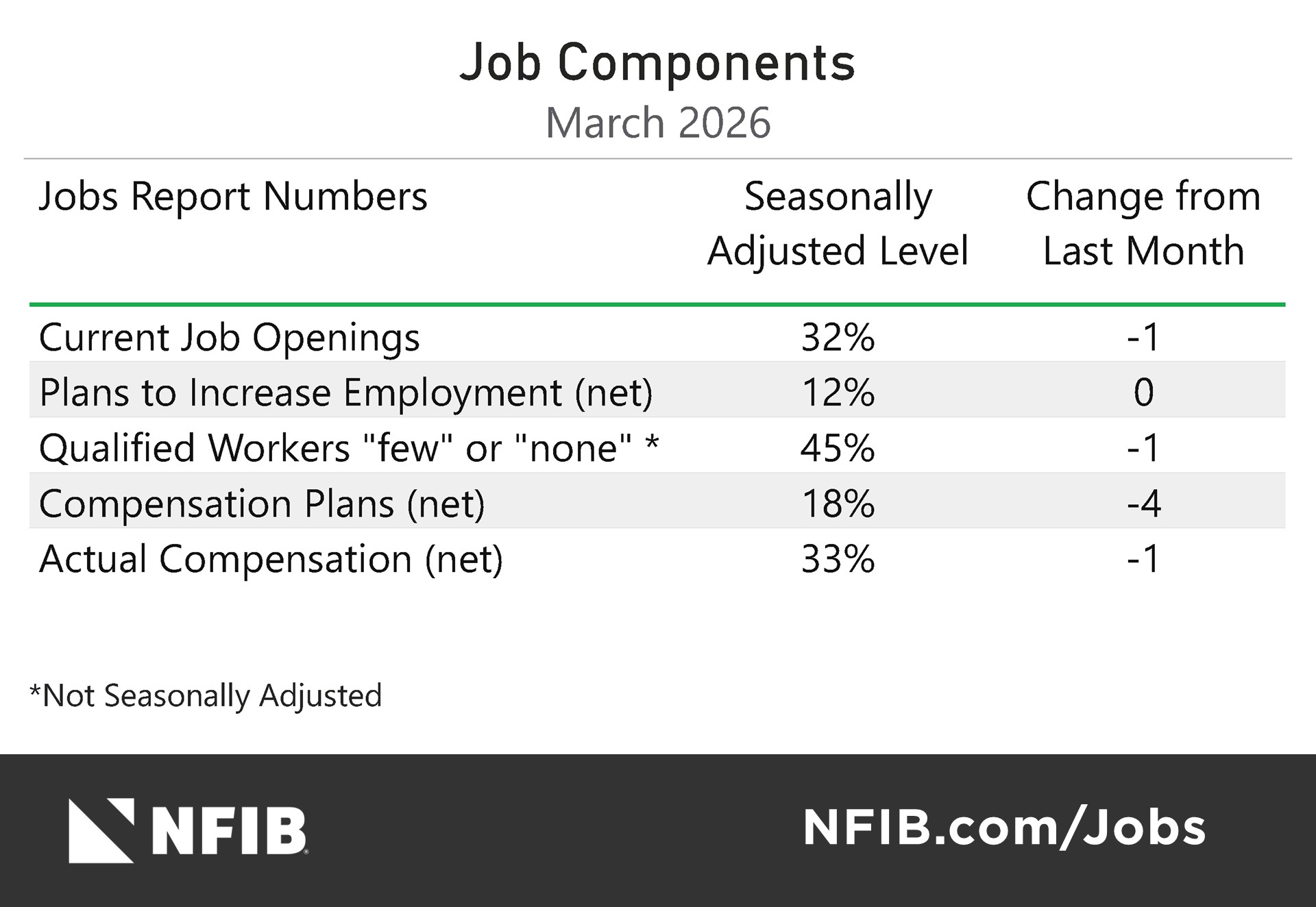

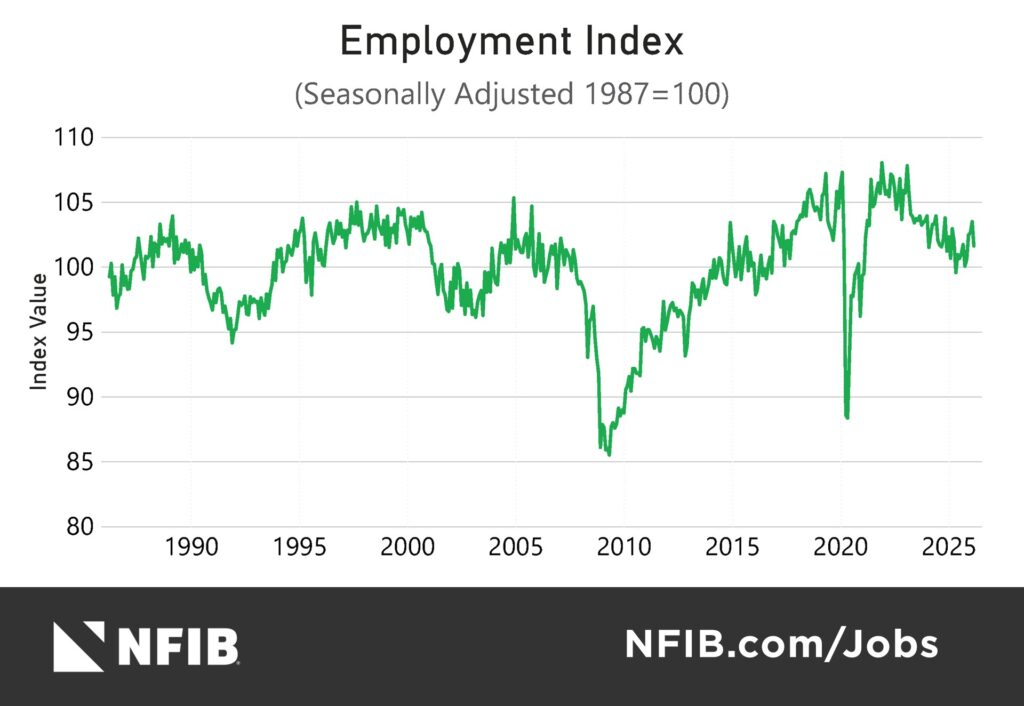

The Employment Index fell in March from 103.5 to 101.6. While the 1.9-point decline is a meaningful turn in labor market conditions, the current reading remains above both the 2025 average of 101.2 and the historical average of 100.

In March, both planned and actual labor compensation decreased from the previous month. A seasonally adjusted net 33% reported raising compensation, down 1 point from February. A seasonally adjusted net 18% plan to raise compensation in the next three months, down 4 points from February and the lowest reading since July 2025.

Sixteen percent (seasonally adjusted) of small business owners plan to make capital outlays in the next six months, down 2 points from February and the lowest level since November 2009.

A seasonally adjusted net negative 5% of all owners reported higher nominal sales in the past three months, down 6 points from February. This decline ended a string of four consecutive months of improvement.

A net negative 5% (seasonally adjusted) of owners plan inventory investment in the coming months, down 3 points from February and the lowest level since May 2024. This is in step with the decline in those expecting higher sales over the next quarter.

In March, 62% of small business owners reported that supply chain disruptions affected their business to some extent, up 3 points from February. Three percent reported a significant impact (down 2 points), 17% reported a moderate impact (up 3 points), 42% reported a mild impact (up 2 points), and 36% reported no impact (down 3 points).

Actual price increases picked up in March following three consecutive months of decline. The net percent of owners raising average selling prices rose 1 point from February to a net 25% (seasonally adjusted), well above its historical average.

In contrast to actual prices, planned prices declined in March, falling 4 points to a net 24% (seasonally adjusted). This was the lowest level since July 2024.

When asked to evaluate the overall health of their business, 13% rated it as excellent (up 1 point), 51% as good (down 4 points), 30% as fair (up 4 points), and 4% as poor (down 1 point).

The Employment Index fell in March, from 103.5 to 101.6. While the 1.9-point decline is a meaningful turn in labor market conditions, the current reading remains above both the 2025 average of 101.2 and the historical average of 100. In March, 32% (seasonally adjusted) of all owners reported job openings they could not fill in the current period, down 1 point from February. Unfilled job openings remain above the historical average of 24%. Twenty-seven percent had openings for skilled workers (down 1 point), and 12% had openings for unskilled labor (up 2 points). Looking ahead, a seasonally adjusted net 12% of owners plan to create new jobs in the next three months, unchanged from February and close to the average of net 11%. Overall, 52% reported hiring or trying to hire in March, down 2 points from February. Forty-five percent of owners (87% of those hiring or trying to hire) reported few or no qualified applicants for the positions they were trying to fill (down 1 point). Twenty-two percent of owners reported few qualified applicants for their open positions (down 3 points), and 23% reported none (up 2 points). In March, 15% of small business owners cited labor quality as their single most important problem, unchanged from February and above the historical average of 12%. The last time labor quality was reported as the single most important problem by less than 15% was in December 2016. While labor quality has declined as a top problem over the past few months, reports of labor costs as the single most important problem have gradually increased. Ten percent of business owners reported labor costs as their single most important problem, up 1 point from February.

In March, both planned and actual labor compensation decreased from the previous month. Despite these declines, planned and actual labor compensation levels remain above their historical averages of a net 16% and a net 24%. A seasonally adjusted net 33% reported raising compensation, down 1 point from February. A seasonally adjusted net 18% plan to raise compensation in the next three months, down 4 points from February and the lowest reading since July 2025.

Fifty-one percent of small business owners reported making capital outlays in the last six months, down 3 points from February. Actual capital expenditure levels have declined by 9 points since the beginning of this year and remain below the historical average. Of those making expenditures, 36% reported spending on new equipment (down 1 point), 22% acquired vehicles (down 6 points), and 14% improved or expanded facilities (down 1 point). Nine percent spent money on new fixtures and furniture (down 1 point), and 5% acquired new buildings or land for expansion (unchanged). Sixteen percent (seasonally adjusted) of small business owners plan to make capital outlays in the next six months, down 2 points from February and the lowest level since November 2009.

A seasonally adjusted net -5% of all owners reported higher nominal sales in the past three months, down 6 points from February. This marked the first decline following four consecutive months of improvement. As actual sales volume fell in March, so did sales expectations. The net percent of owners expecting higher real sales volumes over the next quarter fell 1 point from February to a net 7% (seasonally adjusted). The net percent of owners reporting inventory gains fell 3 points to a net -6% (seasonally adjusted). Not seasonally adjusted, 7% reported increases in stocks (down 3 points), and 16% reported reductions (down 2 points). A net -5% (seasonally adjusted) of owners viewed current inventory stocks as “too low” in March, down 3 points from February. A net -5% (seasonally adjusted) of owners plan inventory investment in the coming months, down 3 points from February and the lowest level since May 2024. In March, 62% of small business owners reported that supply chain disruptions affected their business to some extent, up 3 points from February. Three percent reported a significant impact (down 2 points), 17% reported a moderate impact (up 3 points), 42% reported a mild impact (up 2 points), and 36% reported no impact (down 3 points).

The frequency of reports of positive profit trends fell 11 points from February to a net -25% (seasonally adjusted), contributing the most of all 10 components to the Optimism Index’s decline. Among owners reporting lower profits, 32% blamed weaker sales, 19% cited the usual seasonal change, and 11% cited price change from their product(s) or service(s). Ten percent cited rising material costs, 7% cited labor costs, and 7% reported other reasons. Among owners reporting higher profits, 53% cited sales volume, 12% cited usual seasonal change, 9% cited labor costs, and 9% cited price change from their product(s) or service(s) as the source of the gain.

In March, the net percent of owners expecting easier credit conditions remained at a net -5% (seasonally adjusted). A net 5% reported their last loan was harder to get than in previous attempts, unchanged from February and close to the historical average of a net 6%. In March, a net -3% of owners reported paying a higher interest rate on their most recent loan, unchanged from February. The average interest rate paid on short maturity loans was 7.9% in March, down 0.3 points from February. Twenty-four percent of all owners reported borrowing regularly, down 1 point from February.

Actual price increases picked up in March following three consecutive months of decline. The net percent of owners raising average selling prices rose 1 point from February to a net 25% (seasonally adjusted), well above its historical average. Unadjusted, 38% reported higher average prices (up 3 points), and 11% reported lower average selling prices (unchanged). Looking forward to the next three months, a net 24% (seasonally adjusted) plan to increase prices, down 4 points from February. The last time price plans were this low was July 2024. Fourteen percent of owners reported that inflation was their single most important business problem, up 2 points from February and ranking third among the top issues.

When asked to evaluate the overall health of their business, 13% rated it as excellent (up 1 point), 51% as good (down 4 points), 30% as fair (up 4 points), and 4% as poor (down 1 point). The net percent of owners expecting better business conditions fell 7 points from February to a net 11% (seasonally adjusted). This was the third consecutive monthly decline in expected business conditions and the lowest level since October 2024. In March, 11% (seasonally adjusted) reported that it is a good time to expand their business, down 4 points from February and falling below its historical average. This marked the first decline in six months.

In March, 19% of small business owners reported taxes as their single most important problem, unchanged from February and ranking as the top problem. Taxes have ranked as the top issue far more often than other issues like labor quality, inflation, and poor sales which are not currently in a bad state. In March, 15% of small business owners cited labor quality as their single most important problem, unchanged from February and ranking as the second top issue. The last time labor quality was reported as the single most important problem by less than 15% was in December 2016. While labor quality has declined as a top problem over the past few months, reports of labor costs as the single most important problem have gradually increased. Ten percent of business owners reported labor costs as their single most important problem, up 1 point from February. Fourteen percent of owners reported that inflation was their single most important business problem, up 2 points from February. Inflation ranked third among the top issues, and was 7 points above its historical average. The percent of small business owners reporting poor sales as their top business problem fell 1 point to 10%. In March, 9% reported the cost or availability of insurance as their single most important problem, unchanged from February. The percent of small business owners reporting government regulations and red tape as their single most important problem fell 3 points from February to 7%. Seven percent reported competition from large businesses as their single most important problem, down 1 point from February. Three percent reported that financing and interest rates were their top business problem in March, down 1 point from February.

Overview

The government reported 178,000 new jobs in March, but February and January were collectively down by almost as many jobs, and will likely be revised lower as have prior months. Federal government employment continued to fall but private job creation was a real positive, with 26,000 jobs in construction and 22,000 in transportation. Small business owners have plenty of job openings but are not optimistic about filling them with qualified workers, and some continue to struggle with finding applicants.

Inflation will become even more of a problem as oil prices respond to developments in the Iran conflict. Only a few ships are getting through Hormuz each day compared to well over 100 pre-war, slowing not only the supply of oil, but many other important products as well. The Federal Reserve is likely to stay steady now, but a rate hike becomes more likely if the current elevated inflation environment persists. The share of small business owners raising average selling prices has stabilized at rates that prevailed at the end of the last administration (CPI up 20% over 4 years). Lower oil prices will benefit all concerned, but that may take a while even after the Strait is reopen.

The 20% Small Business Deduction and other supportive small business tax provisions in the OBBB had many positives for small business owners. The Iran war has taken the eye off the ball and spooked consumers and owners alike. A resolution of the conflict will eliminate supply chain problems, lower the price of oil, and all other related products. In the meantime, uncertainty reigns.

Quotes – NFIB Members

Inflation has caused significant hardship in rebalancing our budget. Not only do supplies cost more, labor is expensive with the Michigan minimum wage increase. Between inflation and rising minimum wage, the future of our business is not as certain as it once was.” – Services, MI

“Health insurance is another major issue facing my business. Our problem is not enough employees to getva group policy.” – Retail, PA

“Business is slow! It is getting harder to pay back our line of credit. Some customers are slow to pay.” – Services, OK

“I have 40+ years of experience with 30 years as an owner and our biggest obstacles are taxes and insurance. Our biggest fear is government. Governmental red tape is also a problem. Requiring business owners to respond to audits and surveys is also frustrating as our time should be spent growing our business.” – Retail, MT

“We pay taxes on everything. Every time I turn around, I am paying taxes- paid to buy [the] building then, pay every year to have the building that I own, pay taxes on payroll, sales tax, quarterlies, and income tax.” – Retail, PA

“The overall state of my business is good at the moment, however with all the uncertainty in the economy (tariff surcharges, high freight charges, skyrocketing insurance rates, and the war with Iran), I feel to cover the increased cost I may price myself out of the market. Lowering prices is only an option if prices of inputs come down and that doesn’t look like it will happen in the near future.” – Retail, IA

“Government regulations are a hindrance to say the least.” – Services, MD

“Cannot compete with online retailers like Amazon, Walmart, etc.” – Retail, TX

“[The] cost of seed, chemicals, and fertilizer has gone way up. Replacement costs of farm machinery have doubled in the last five years. Without government subsidies, there are not many crop farmers making any money [in] the last two years. If this keeps up, there will be farmers forced by their lenders to retire. Government payments help all farmers financially, but it is not a long-term fix. We need competition in the marketplace for our crop farming inputs or [to] increase our biofuel usage in this country.” – Agriculture,

MN

“Sales are down, and customers are extremely price conscious.” – Agriculture, NJ

“The cost of qualified skilled labor is high. Too high for the level of skill the labor force has. Benefits are toocostly on top of high wages. Goods from manufacturing cannot just simply raise the price because ourcustomers will buy from Mexico or China instead of paying more for U.S. made. It’s a tough market, and the losers are the American worker and small business owner. – Manufacturing, MI

“I fear AI will take over some of my customers’ jobs and have an effect on recreational sales and some disposable income in the tourism-driven business.” – Services, NH

“Since I own and operate a financial services company, I do not have the ability to increase revenue other than [by] bringing new clients to our firm. This is a necessity to keep up with increases in salaries and other expenses such as marketing, utilities, and others.” – Financial, TX

“Online/Amazon sales are ever increasing and taking more sales (everyday average type sales) from brickand-mortar stores. The day is quickly coming when a particular market will no longer be able to support several same type businesses within a market. Since Amazon is taking more from everyone (brick-andmortar), the pie is shrinking.” – Retail, WA

“[The] cost of goods overall has increased (but seems to be leveling). Being a small business, it is very difficult to provide medical insurance with the higher cost of goods and services. The average working person finds it difficult to pay for many goods and services with the current economy we have due to overprinting the currency.” – Construction, AZ

“We deal with surveying housing. The cost of building supplies and interest rates have to drop a lot. Cost of food has to go down. If this doesn’t [happen] we won’t make it!” – Profession/ business services, CO

As reported in NFIB’s monthly jobs report, the NFIB Small Business Employment Index fell 1.9 points from February to 101.6. This decline is indicative of further moderation in the labor market. February’s data was discussed on a newly released episode of the NFIB Research Center’s “Small Business by the Numbers” podcast. Listen to the latest episode here.

A seasonally adjusted 32% of small business owners reported job openings they could not fill in March, down 1 point from February. Unfilled job openings remain above the historical average of 24%. Twenty-seven percent had openings for skilled workers (down 1 point), and 12% had openings for unskilled labor (up 2 points).

Looking ahead, a seasonally adjusted net 12% of owners plan to create new jobs in the next three months, unchanged from February and close to the average of a net 11%. Overall, 52% of owners reported hiring or trying to hire in March, down 2 points from February. Forty-five percent of owners (87% of those hiring or trying to hire) reported few or no qualified applicants for the positions they were trying to fill (down 1 point). Twenty-two percent of owners reported few qualified applicants for their open positions (down 3 points), and 23% reported none (up 2 points).

In March, both planned and actual labor compensation decreased from the previous month. Despite these declines, planned and actual labor compensation levels remain above their historical averages. A seasonally adjusted net 33% reported raising compensation, down 1 point from February. A seasonally adjusted net 18% plan to raise compensation in the next three months, down 4 points from February and the lowest reading since July 2025. While both planned and actual labor compensation decreased in March, compensation levels remain above their historical average.

Fifty-one percent of owners reported capital outlays in the last six months, down 3 points from February. Actual capital expenditure levels have declined by 9 points since the beginning of this year and remain below the historical average. Of those making expenditures, 36% reported spending on new equipment, 22% acquired vehicles, and 14% improved or expanded facilities. Nine percent spent money on new fixtures and furniture and 5% acquired new buildings or land for expansion.

A seasonally adjusted net negative 5% of all owners reported higher nominal sales in the past three months, down 6 points from February. This marked the first decline following four consecutive months of improvement. The net percent of owners expecting higher real sales volumes over the next quarter fell 1 point from February to a net 7% (seasonally adjusted).

The net percent of owners reporting inventory gains fell 3 points from February to a net negative 6%, seasonally adjusted. Not seasonally adjusted, 7% reported increases in stocks and 16% reported reductions. A net negative 5% (seasonally adjusted) of owners viewed current inventory stocks as “too low” in March, down 3 points from February. A net negative 5% (seasonally adjusted) of owners plan inventory investment in the coming months, down 3 points from February and the lowest level since May 2024.

Actual price increases picked up in March following three consecutive months of decline. The net percent of owners raising average selling prices rose 1 point from February to a net 25% (seasonally adjusted), well above its historical average.

The frequency of reports of positive profit trends fell 11 points from February to a net negative 25% (seasonally adjusted). Among owners reporting lower profits, 32% blamed weaker sales, 19% cited usual seasonal change, and 11% cited price change from their product(s) or service(s). Ten percent cited rising material costs, 7% cited labor costs, and 7% reported other reasons. For owners reporting higher profits, 53% cited sales volume, 12% cited usual seasonal change, 9% cited labor costs, and 9% cited price change from their product(s) or service(s) as the source of the gain.

In March, the net percent of owners expecting easier credit conditions remained at a net negative 5% (seasonally adjusted). A net 5% reported their last loan was harder to get than in previous attempts, unchanged from February and close to the historical average of net 6%. A net negative 3% of owners reported paying a higher interest rate on their most recent loan, unchanged from February. The average interest rate paid on short maturity loans was 7.9% in March, down 0.3 points from February. Twenty-four percent of all owners reported borrowing regularly, down 1 point from February, a historically weak reading.

In March, 11% (seasonally adjusted) reported that it is a good time to expand their business, down 4 points from February and falling below its historical average. This marked the first decline in six months.

Nineteen percent of business owners reported taxes as their single most important problem, unchanged from February and ranking as the top problem. Fifteen percent of owners cited labor quality as their single most important problem, unchanged from February and ranking as the second top issue. Fourteen percent of owners reported that inflation was their single most important business problem, up 2 points from February and ranking as the third top issue.

The NFIB Research Center has collected Small Business Economic Trends data with quarterly surveys since the fourth quarter of 1973 and monthly surveys since 1986. Survey respondents are randomly drawn from NFIB’s membership. The report is released on the second Tuesday of each month. This survey was conducted in March 2026.